Transaction Center

Time to bring it home. Find zipForm®, transaction tools, and all the closing resources you'll need. Except for the champagne — that's on you.

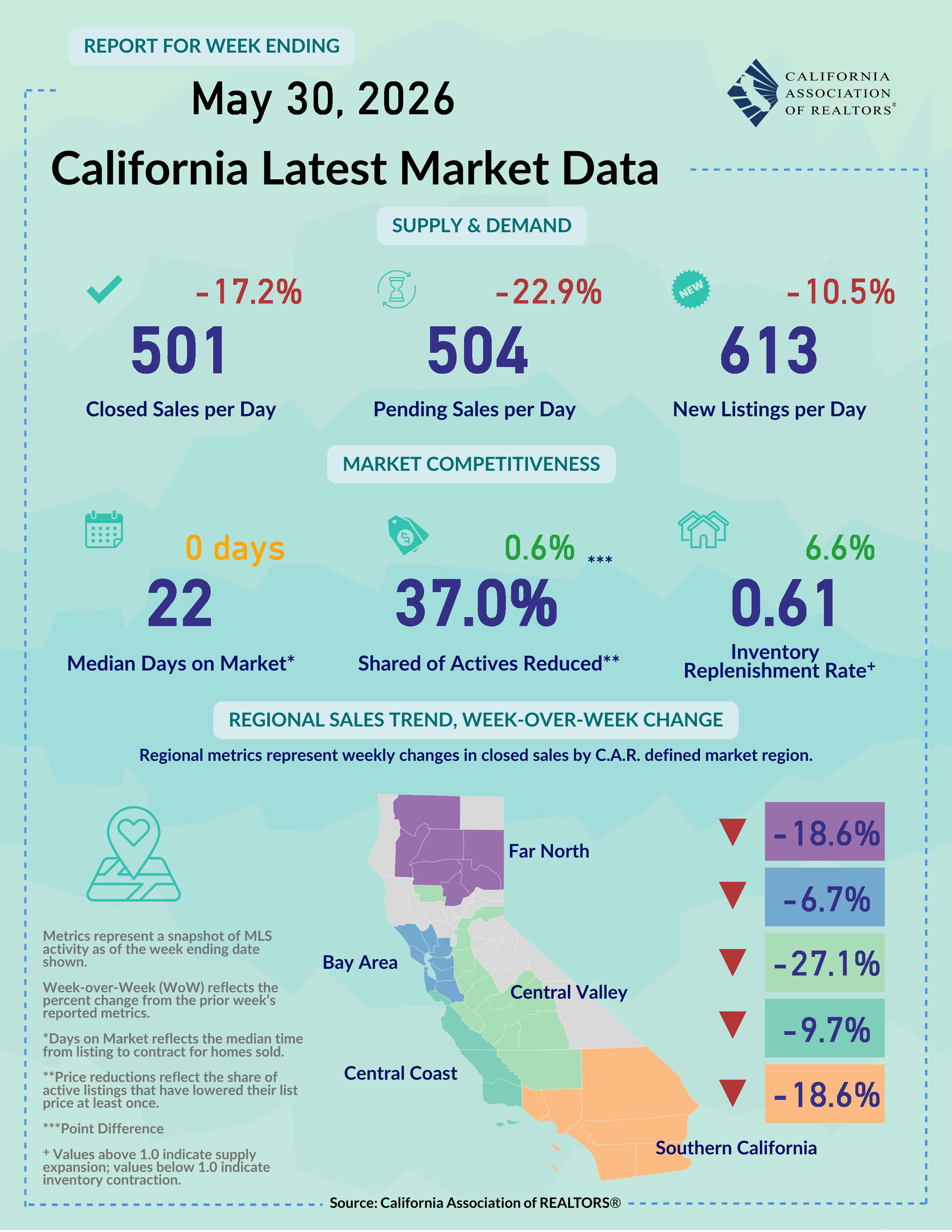

View the latest sales and price numbers. Find out where sales will be in upcoming months.

Get a roundup of weekly economic and market news that matters to real estate and your business.

Gain insights through interactive dashboards and downloadable infographic reports.

All Shareable Reports All Interactive DashboardsCatch up with the latest outreaches and webinars by the Research and Economics team.

C.A.R. conducts survey research with members and consumers on a regular basis to get a better understanding of the housing market and the real estate industry.

California Model MLS Rules, Issues Briefing Papers, and other articles and materials related to MLS policy.

Looking for information on how to file an interboard arbitration complaint? You've come to the right place! Find the rules, timeline and filing documents here.

Summaries and photos of California REALTORS® who violated the Code of Ethics and were disciplined with a fine, letter of reprimand, suspension, or expulsion.

The most recent edition of the Code of Ethics and Standards of Practice of the National Association of REALTORS® along with other important links to NAR information.

The California Professional Standards Reference Manual, Local Association Forms, NAR materials and other materials related to Code of Ethics enforcement and arbitration.

C.A.R. advocates for REALTOR® issues in Washington D.C., Sacramento and in city and county governments throughout California.

CREPAC, LCRC, IMPAC, ALF and the RAF comprise C.A.R.'s political fundraising arm.

The RAA: Protecting REALTORS® and Homeownership REALTOR® Action FundC.A.R. Senior Vice President Sanjay Wagle sits down with former Senate Majority Leader Emeritus Robert Hertzberg to discuss the proposed Middle-Class Homeownership and Family Home Construction Act.

Learn how you can make a difference, by getting involved yourself or by passing along valuable information to your clients.

|

June 01, 2026 – Despite soft economic fundamentals and fragile sentiment, the outlook for the second half of the year could still improve if geopolitical tensions in the Middle East ease and the Iran conflict moves toward a resolution. Recent data suggest that consumers and business leaders remain cautious as inflation, high borrowing costs, and uncertainty continue to weigh on confidence. Even so, a de-escalation in the U.S. - Iran war would likely reduce pressure on energy markets, help stabilize inflation expectations, and support a better macroeconomic environment in the months ahead. Within housing, elevated mortgage rates and growing inventories weighed on new home sales, while the rental market continued to benefit from abundant apartment supply, keeping rent growth subdued despite seasonal demand. Collectively, these trends suggest that affordability challenges remain a key constraint for California's housing market. Housing conditions, nevertheless, could see some gradual improvement over the next six months as market adjustment continues and buyer activity slowly gains traction. Consumer Sentiment Falls to Historic Lows as Inflation Concerns Weigh on Household Outlook, Though Spending Remains Resilient: Consumer attitudes toward the economy weakened further in May, with the University of Michigan’s consumer sentiment index falling to its lowest level on record as concerns over inflation, rising fuel costs, and broader economic uncertainty intensified. While economists caution that sentiment measures do not always translate directly into spending behavior, the deterioration highlights growing household unease about personal finances and future economic conditions. Despite the decline in confidence, consumer spending has remained relatively resilient, supported by low unemployment, steady wage growth, and accumulated household wealth. Looking ahead, persistent inflation pressures will likely lead to consumers prioritizing essential purchases over discretionary spending which could soften overall personal expenditures, but recent retail sales trend suggests that any slowdown in spending may be more gradual than sentiment surveys imply. CEO Confidence Plunged in the Second Quarter as Business Risks Rise: Corporate leaders’ optimism declined sharply in the latest quarterly survey conducted by the Conference Board. The CEO Confidence Index tumbled by 12 points to 47 in Q226 from 59 in Q126, reversing the upward trend observed earlier in the year. Nearly half (47%) of all CEO’s said economic conditions were worse, up from just 8% in the first quarter. In the short term, 40% of them expected the economy to get worse, a jump from 13% last quarter. Their concerns about cyber risks for their industry continued to rise in Q226 to 65% from 56% in the prior quarter, while geopolitics (62%) and AI/new technology (57%) remained their top business risks. Worries about supply chains (36%) and energy supply (34%) surged significantly in the second quarter, likely due to the Middle East conflict. With the U.S/Iran negotiation yet to be settled, CEO confidence could remain subdued until an agreement to end the war is reached. Consumer Spending Seemingly Holds Up as Inflation Hikes and Savings Rate Falls to Near-Four-Year Low: Consumer spending rose in April, but the financial backdrop suggests households are becoming increasingly stretched. Personal spending increased 3.8% from a year ago as core PCE inflation accelerated by 3.3% year over year, while the personal saving rate fell to 2.6%, its lowest level since mid-2022. While resilient spending continues to support economic growth, declining savings and softer real income gains may make it more difficult for prospective homebuyers to accumulate down payments and absorb higher housing costs, particularly in high-priced markets such as California. Persistent inflation also reinforces the Federal Reserve’s cautious approach to policy rate movements, limiting the potential for meaningful mortgage-rate relief in the near term. New Home Sales Miss Expectations in April as Higher Mortgage Rates Keep Demand Down: Sales of newly constructed single-family homes in the U.S. declined 6.2% in April to a seasonally adjusted annual rate of 622,000, falling well below expectations of 660,000, as elevated mortgage rates and economic uncertainty continued to weigh on buyer demand. April new housing purchases were 6.2% below March’s sales pace and were down 11.3% from the level recorded in April 2025. Three of four regions in the U.S. experienced double-digit year-over-year declines, and the West was only bright spot with an increase of 4.6% from the year-ago level. With sales slowing, new-home inventory climbed to its highest level in years, pushing months of supply to 9.4 months from 8.7 months in March and 8.6 months in April 2025. Despite a tick-up in months of inventory, for-sale new housing units actually dipped 2.2% from a year ago as builders pulled back on new housing construction due to their concerns of growing backlog of unsold homes. For California, where affordability remains a challenge, rising inventory and slower demand will put a cap on home price growth, and builders will likely continue to rely on incentives and price adjustments to attract buyers. Apartment Rents Post Seasonal Gains but Elevated Supply Keeps Annual Growth in the Negative: The rental market continued to stabilize this spring, with the national median rent rising 0.5% in May to $1,379 as seasonal leasing activity strengthened. Despite four consecutive monthly increases, rents remained 1.5% below year-ago levels and 4.4% below their 2022 peak, reflecting the lingering effects of a historic wave of newly constructed multifamily units over the past years. While elevated apartment inventory continues to restrain rent growth and limit landlords’ pricing power, the rental market is showing a glimpse of improvement as the national vacancy rate continued to moderate after reaching a new record high in February. While the market is showing an encouraging sign of finally turning the corner, geopolitical risks and economic uncertainty will likely present challenges to the recovering rental demand in the coming months. Note: This summary report gets updated every Monday by 6:00 pm PST. Feel free to email us at [email protected] if you have any questions and/or feedback.

|

|